Is a team of legal specialists who will assist you in opening a company and provide other legal services necessary for developing your business in Lithuania. We will introduce you to the legal environment of Lithuania as soon as possible.

WE OFFER

Three possible options to register a company in Lithuania starting from 1,000 EUR

All companies and subsidiaries in Lithuania are subject to the obligation to keep accounts

Lithuanian government offers transparent and cost-effective virtual currency authorization

ABOUT US

Company in Lithuania UAB – is a team of lawyers, paralegals, and legal advisors who will help you open a company and develop your business in Lithuania. We will gladly familiarise you with the legal environment of Lithuania as soon as possible.

In addition to establishing companies, legal services, and accounting services, we offer our clients assistance in obtaining crypto license and other financial licenses and recruiting personnel.

We are a multilingual company and can communicate with you in several languages, so we can answer all your questions about doing business in Lithuania in your preferred language!

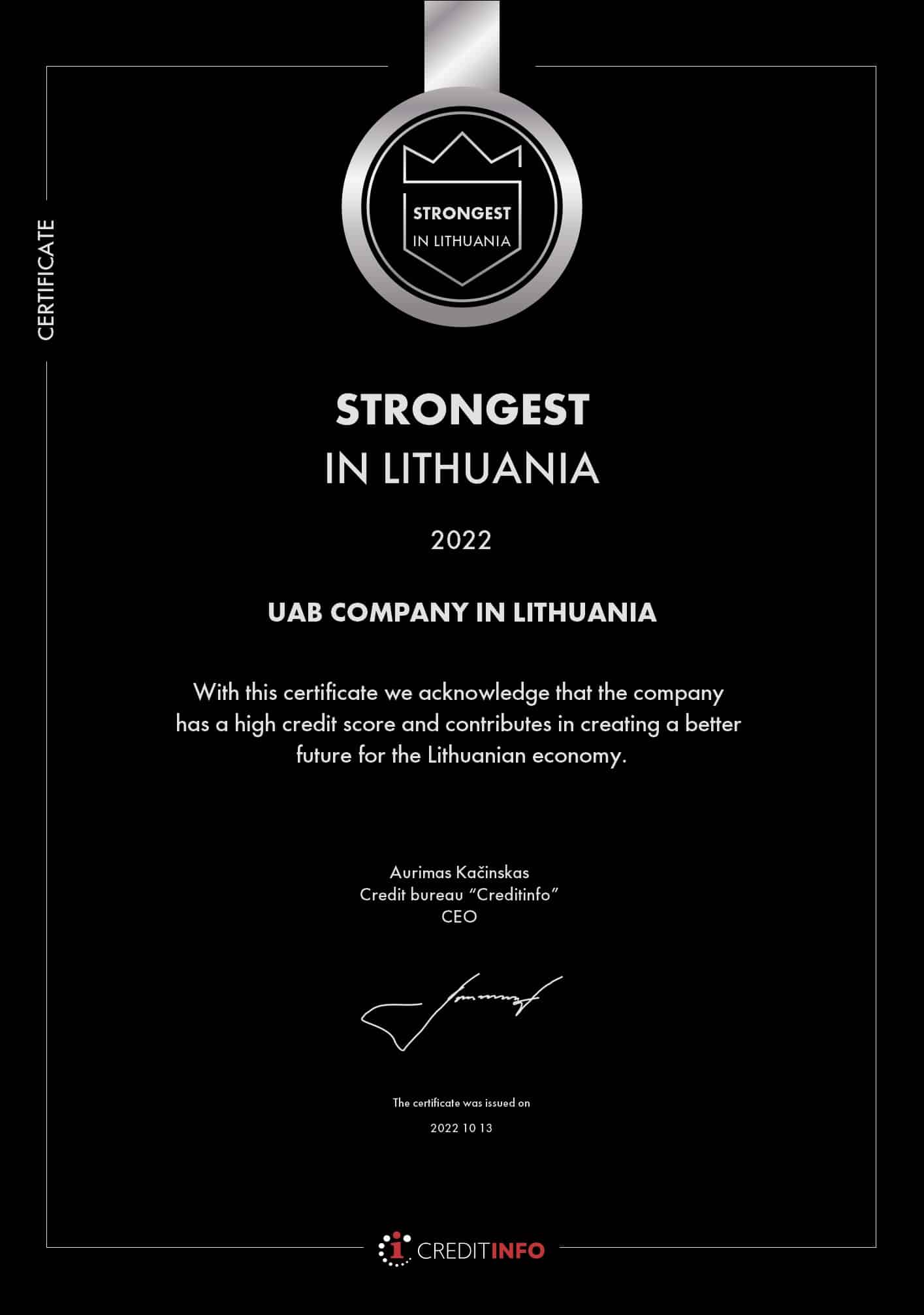

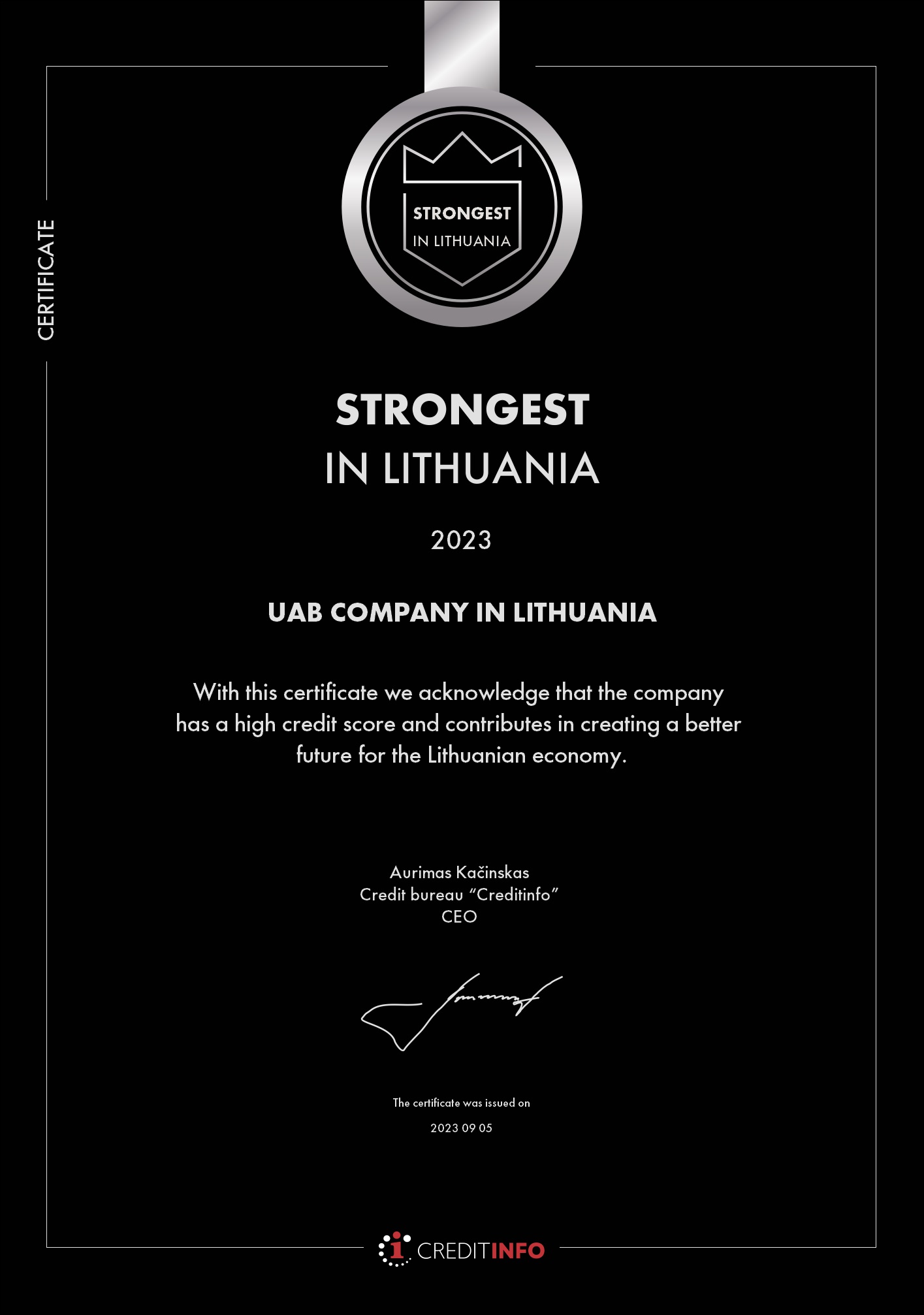

Company in Lithuania UAB is contributing to the economy of the Lithuanian Republic every day and promoting an honest business culture. Based on the economic data of 2021, our company has received a high credit rating score and been granted the Strongest in Lithuania 2022 designation.

Company in Lithuania UAB

OUR VALUES

Innovation

Quickly and effectively, the digital environment and openness to financial innovation made Lithuania a starting point for the realization of new and bold business ideas for entrepreneurs from all over the world. For us it is important to expand the established corporate borders and provide new start-up opportunities for our clients from all corners of the world. We hope to contribute new value to the formation of international business, basing our principles on the unlimited possibilities of Lithuania in the era of its technological rise and simple business decisions, which are at a distance of one click!

Teamwork

We understand that the efficiency of our work depends on the personal contribution of each of the Company in Lithuania UAB team. That’s why our team’s vision is based on mutual assistance and daily teamwork. We are encouraged by the interaction with our clients, partners and colleagues. We understand our mission and integrate corporate values into all aspects of our business. One of the fundamental pillars of our success lies in setting achievable goals, corporate responsibility for team decisions and bringing the projects started to fruition.

Individual approach

We are proud of the fact that our clients have different ethnic identities and see in their mission the general integration in the front line of Lithuanian business. We are quick to respond to the industry’s volatility and the variety of challenges we face. Furthermore, we strictly adhere to professional ethics, as we are convinced that they are necessary for effective cooperation. All services provided by us are tailored to the demand of international clients and can be refined on their individual request.

Dynamics

It is no secret that the situation in the world is constantly changing and demands from us rapid and effective solutions. Therefore, in Company in Lithuania UAB we are in step with the time. We value our clients’ time, so Company in Lithuania UAB’s corporate, accounting and legal services are provided as quickly as possible. In a volatile environment, a firm’s performance determines its success. It is important for us to provide quality service in the shortest possible time, and therefore, we answer all requests of our clients within a few hours.

1

COMPANIES

1

CLIENT COUNTRIES

1

SPECIALISTS

1

YEARS IN MARKET

Our blog

Company in Lithuania UAB has a blog where the latest Lithuanian economic and business news is published. We base our articles on topics that are essential for entrepreneurs, new business developments and interesting projects. If you cannot find the information you are looking for in our blog, please contact us in a way that is convenient for you.

Company in Lithuania UAB partners

Company in Lithuania UAB has a blog where the latest Lithuanian legal, economic, and business news is published. Our articles focus on topics that are essential for entrepreneurs, new legal and business developments, and interesting projects. If you cannot find the information you are looking for in our blog, please don’t hesitate to contact us using the method that is most convenient for you.